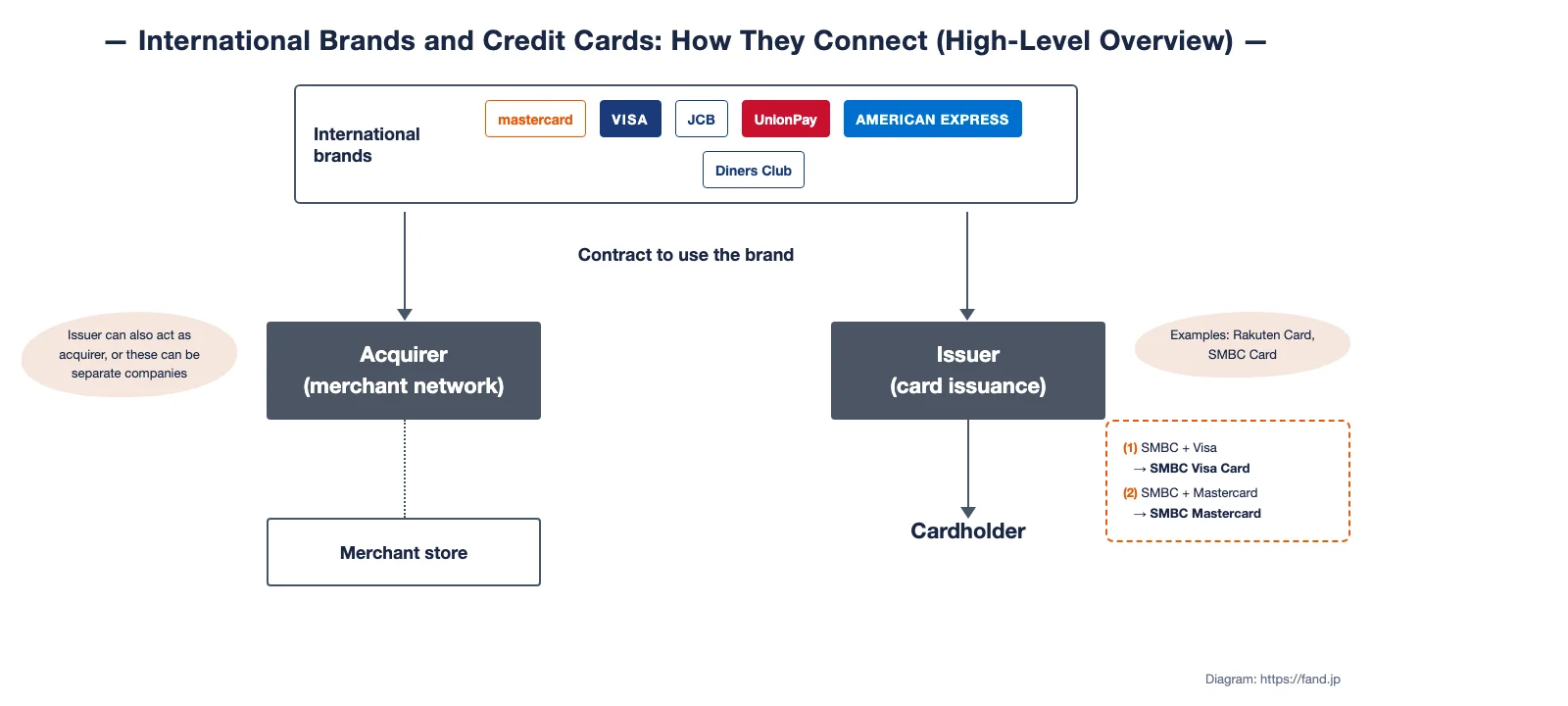

The brand logos on credit cards — what the industry calls “international brands” or, more precisely, payment networks — represent the companies that operate global card processing networks. Visa, Mastercard, Japan’s own JCB, the upmarket American Express and Diners Club, and others. Each network differs in merchant coverage, fee structure and the kind of perks the issued cards tend to come with.

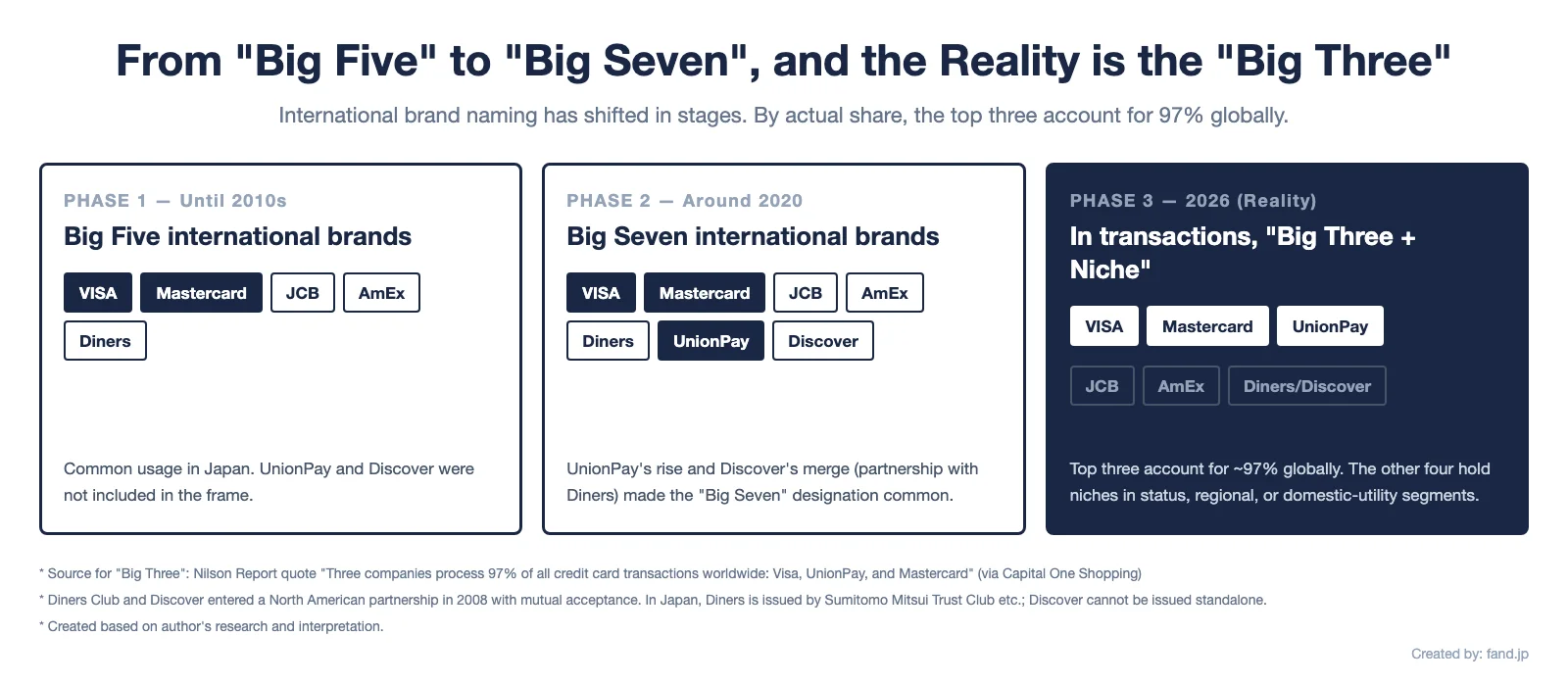

How many “major” networks there are depends on how you count. The traditional Big Five grouping is Visa / Mastercard / JCB / AmEx / Diners Club. A more recent Big Seven view adds UnionPay and Discover. Both groupings coexist in industry references. This article uses the Big Seven framing, and looks at how the actual top-three structure — where Visa, Mastercard and UnionPay together account for roughly 97% of global purchase transactions — has held up between 2020 and the most recent published data.

This article is written from the perspective of a Japan-based card user. It focuses on global payment network share and how that context affects card choice in Japan. It is not a recommendation guide for U.S. or European cards, and Japanese-issued cards mentioned here are generally only available to Japan residents.

The original Japanese version of this article was first published in 2022 and used 2020 Nilson Report data. The 2020 figures are kept as a reference, with updates layered on top using data published in 2024-2025 (Global = Nilson Report H1 2024 / U.S. = Nilson Report 2023 figures / Europe = Statista 2024-2025 estimates). If you are reading this for the year-on-year comparison, the side-by-side tables in each section are the part to skim.

Key takeaways

- Whether you call it “Big Five” or “Big Seven”, in practice Visa, Mastercard and UnionPay together hold roughly 97% of global purchase transactions.

- In the U.S., Visa held a leading share around 52% both in 2020 (entire Payment Cards market) and in 2023 (credit cards only). The two years use different bases, so per-brand point differences cannot be compared directly between them.

- The old “Europe equals Mastercard” intuition no longer fits in 2026. Visa is still ahead in Europe, but Mastercard has narrowed the gap.

- JCB’s merchant network grew from roughly 37 million to about 71 million locations, while its share in regional transaction-volume figures has barely moved.

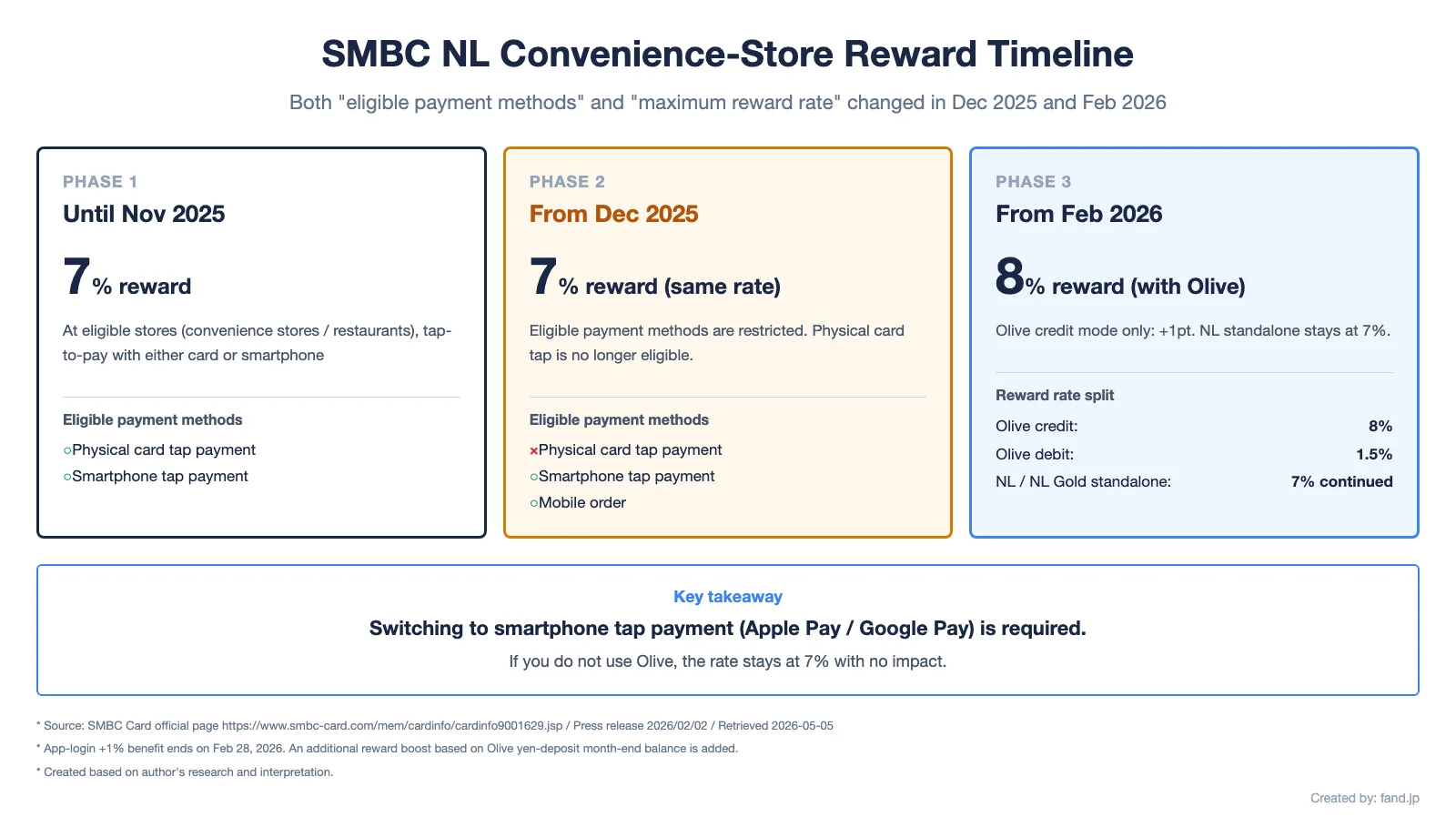

- SMBC’s NL convenience-store 7% reward, starting December 2025, applies only to smartphone touch payments and mobile-order use — physical-card touch payments are no longer included.

What “international brands” actually means

It is the set of brands that allow a credit card to be accepted internationally. The familiar set of logos belongs to that group.

How many networks count as “major” varies by source. The traditional Big Five view — Visa / Mastercard / JCB / AmEx / Diners Club — is the most common. A more inclusive Big Seven view adds UnionPay and Discover; JCB’s official site, for instance, lists seven brands. This article follows the Big Seven framing. As a side note, Discover is not directly issued by Japanese banks; it is interoperable with Diners Club through a partnership.

| Network | Country of origin |

|---|---|

| Visa | United States |

| Mastercard | United States |

| JCB | Japan |

| American Express | United States |

| Diners Club | United States |

| UnionPay | China |

| Discover | United States |

| Network | Notes | Domestic acceptance (Japan) | Overseas acceptance | Status image | Example issuers (Japan) | Origin |

|---|---|---|---|---|---|---|

| Visa | Largest global network. Strong overseas usability. | High | Very high | Mainstream | Sumitomo Mitsui Card, Rakuten Card, etc. | U.S. |

| Mastercard | Second-largest global share. Strong overseas usability. | High | Very high | Mainstream | Rakuten Card, Life Card, etc. | U.S. |

| JCB | Japan-origin network. Strong domestic acceptance. | Very high | More limited (supplemented by partner networks) | Mainstream to premium | JCB Card, Seven Card, etc. | Japan |

| American Express | Premium positioning. | High, but not accepted at every merchant | Wide | Premium | Marriott Bonvoy AmEx, AmEx-issued cards | U.S. |

| Diners Club | Premium positioning, smaller footprint. | Lower | Wide | Premium | Sumitomo Mitsui Trust Club issuance, etc. | U.S. |

| UnionPay | Dominant in China; expanding globally. | Mostly tourist areas | Strong in Greater China; expanding | Mainstream | Chinese financial institutions | China |

The “Big Five vs Big Seven” naming, and the actual “Big Three” reality once you look at share, can be summarised in a single chart.

How card brands map to issuer names

In daily life, people pick credit cards by the issuer brand — names like “Rakuten Card” or “Sumitomo Mitsui Card”. Those are the names of cards offered by issuers, who in turn run on top of one of the networks above. Each issuer differentiates on rewards, perks and fee structure.

The full chain is roughly:

- Network (international brand)

- Acquirer

- Issuer

Is JCB a network or an issuer?

Both. JCB operates the network, and also issues its own cards directly under the JCB ORIGINAL SERIES line.

What a credit card actually does

When choosing a card, the criteria fall into roughly four buckets. The first two — rewards and bundled perks — are the parts that change most depending on lifestyle.

- Payment function

- Limits vary by card grade.

- The shared baseline: any card lets you pay without holding cash.

- Network choice occasionally matters. “I only have a JCB card, but this shop only takes Visa or Mastercard” used to be a more common scenario; in practice it has become rare.

- Bundled insurance

- Coverage you get without paying a separate premium.

- Reward rate

- One of the two main differentiators.

- The “best” answer depends on what you actually spend on.

- Issuer-specific perks

- The other main differentiator.

- Whether airport lounge access or priority boarding is worth anything depends entirely on whether you fly.

- T&E cards like AmEx tilt heavily toward “non-everyday” experiences.

A single card rarely covers all four well. Most heavy users end up splitting their usage across two or three cards rather than trying to consolidate into one.

In my own setup, I use one card per network, with each card assigned a specific role — three cards in total. The detailed selection rationale is in a separate article (Japanese).

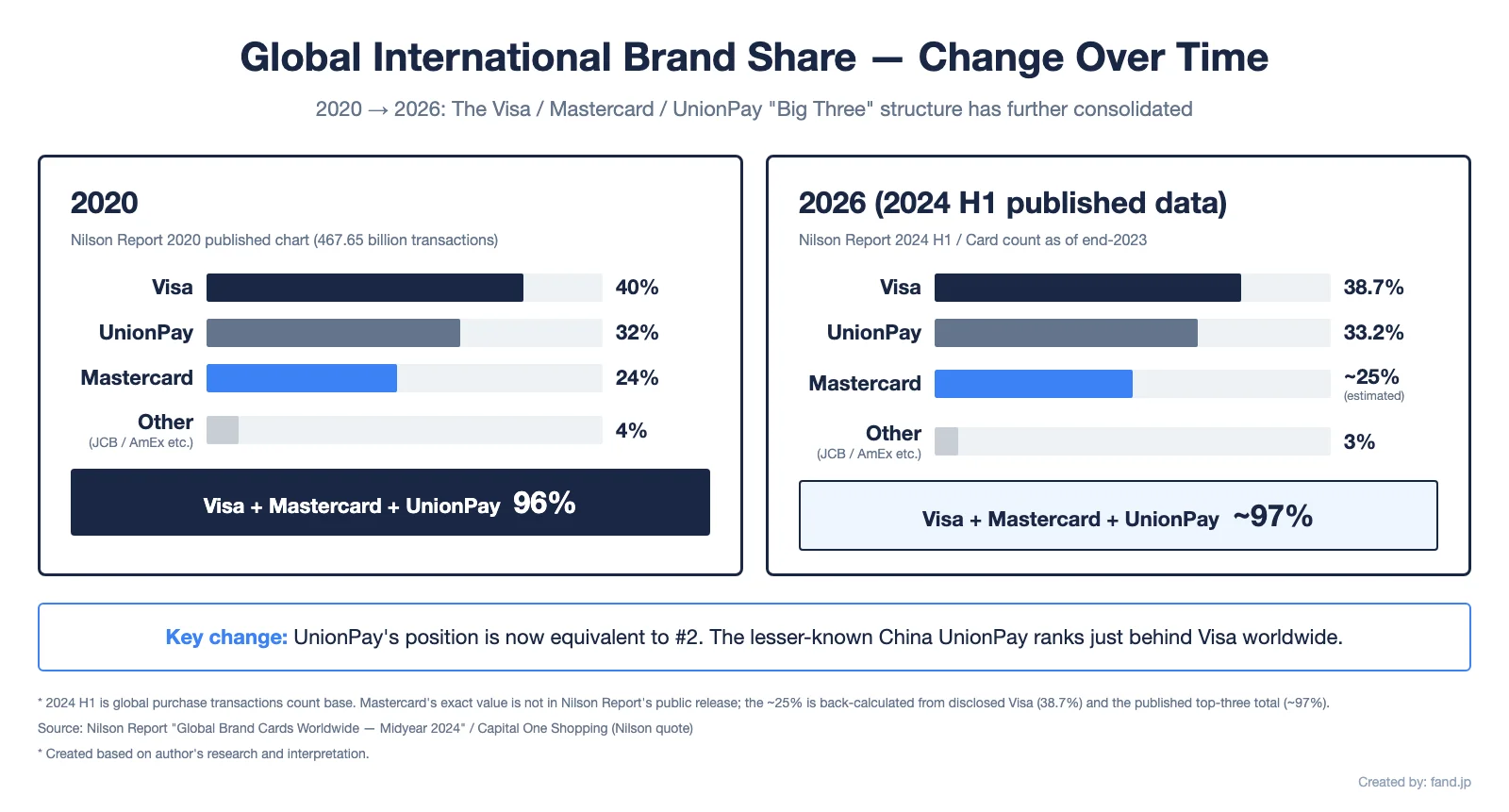

Global share (Nilson Report H1 2024)

Now to the main subject. Using publicly available Nilson Report charts, here is the 2020 global picture, then the most recent published comparison.

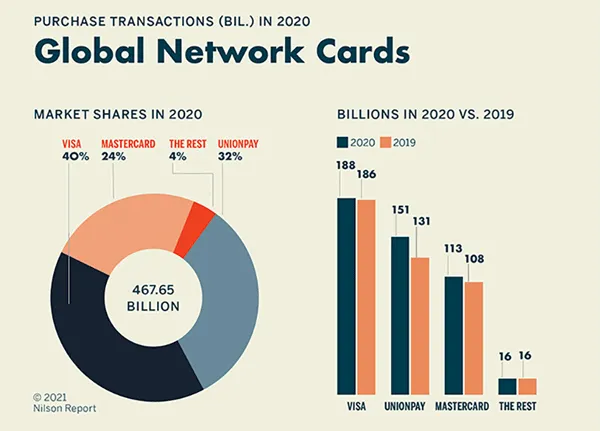

2020 reference numbers

The Nilson Report chart used in the original article showed the following purchase-transaction share, against a total of 467.65 billion transactions.

| Network | 2020 share |

|---|---|

| Visa | 40% |

| UnionPay | 32% |

| Mastercard | 24% |

| Others (JCB / AmEx / Diners, etc.) | 4% |

Visa, Mastercard and UnionPay together accounted for 96% of global purchase transactions.

Card and Mobile Payment Industry Statistics | Nilson Report Archive of Charts & Graphs (© 2021 Nilson Report)

2020 vs H1 2024

The most recent publicly available Nilson Report figure (first half of 2024) shows Visa’s global purchase-transaction share at 38.66% and UnionPay at 33.15%. Mastercard’s exact value is not in the public Nilson Report excerpt, so the 25% figure shown here is an estimate, not a directly published number. The combined share of Visa, Mastercard and UnionPay is widely referenced as roughly 97%, drawing on the public Nilson parts plus secondary-source estimates.

| Network | 2020 share | H1 2024 share | Change |

|---|---|---|---|

| Visa | 40% | 38.7% | -1.3 pt |

| UnionPay | 32% | 33.2% | +1.2 pt |

| Mastercard | 24% | approx. 25% (estimate) | roughly flat |

| Others (JCB / AmEx / Diners, etc.) | 4% | approx. 3% | -1 pt |

| Top 3 combined | 96% | approx. 97% | +1 pt |

Three things to note:

- The Big Three structure is essentially unchanged. Combined top-three share moved from 96% in 2020 to roughly 97% in H1 2024. The four other Big Seven brands (JCB / AmEx / Diners / Discover) together account for around 3% globally.

- UnionPay has overtaken Mastercard for the number-two position by transactions. In 2020 the order was Visa 40% > UnionPay 32% > Mastercard 24%. In H1 2024 it reads Visa 38.7% > UnionPay 33.2% > Mastercard (estimated around 25%). UnionPay, which has limited brand presence in Japan, sits second by transaction volume.

- By number of cards in circulation, UnionPay leads. As of end-2023, UnionPay accounted for roughly 56% of global cards, Visa 25%, and Mastercard 17% (Nilson Report). The size of the Chinese market is the dominant factor.

Note: the 2020 numbers above were read directly from the Nilson Report public chart originally embedded in the Japanese version. The 2026-side Mastercard estimate is back-calculated from “Visa 38.7% + UnionPay 33.2% + top three roughly 97%”. Detailed figures sit behind Nilson’s paid subscription, so the 2026-side numbers combine the public excerpt with secondary-source estimates rather than first-party paid data.

Regional shares (2024-2025 published data)

Network strength varies sharply by region. Below are the 2020 figures alongside the most recent 2024-2025 published estimates and reference values.

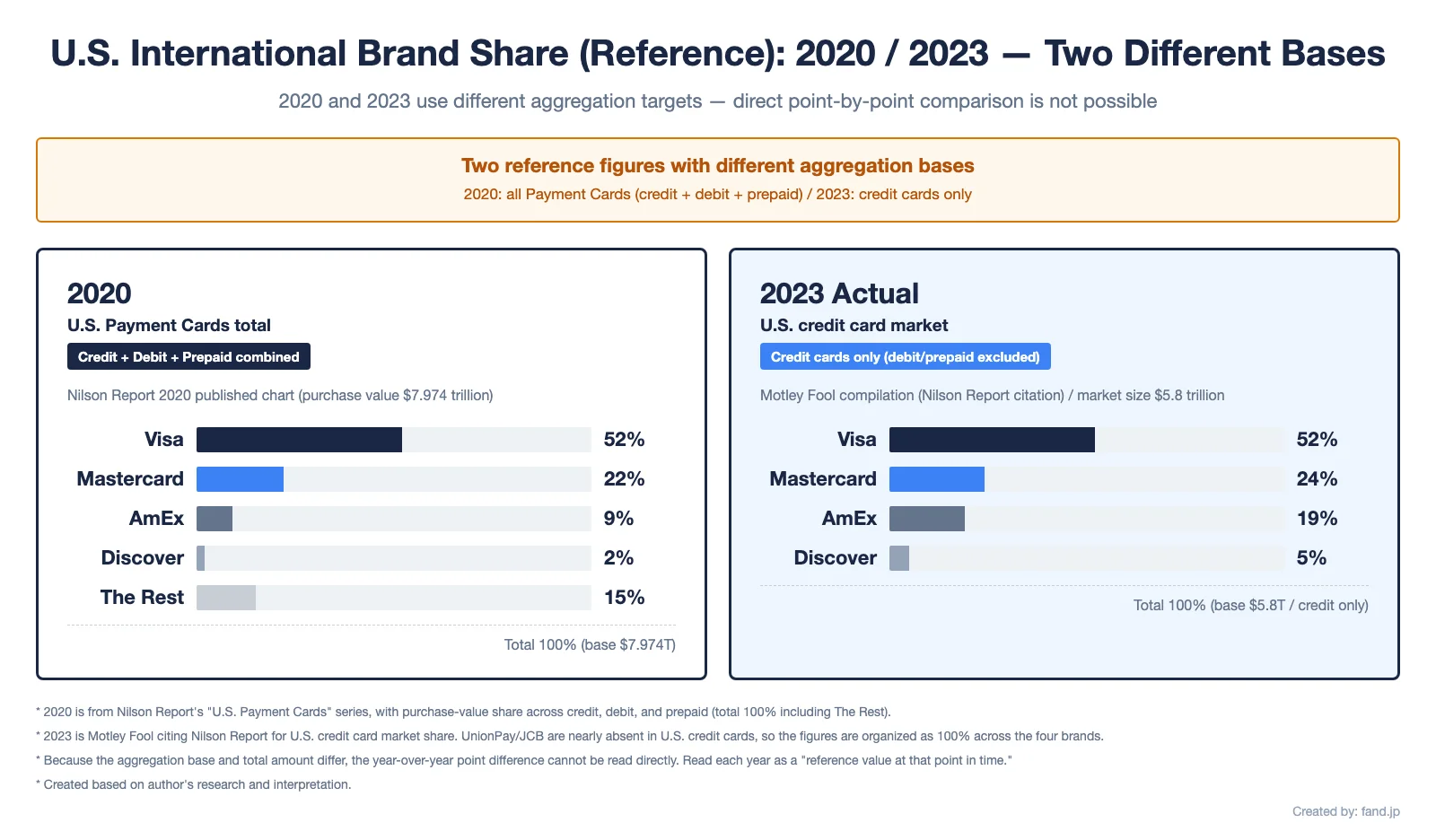

United States: Visa stays ahead, but the 2020 and 2023 bases differ

For the U.S., one important caveat first: the 2020 figures from the original article and the 2023 figures used here are not on the same base. The 2020 numbers are shares of the entire U.S. Payment Cards market — credit, debit and prepaid combined, total purchase volume $7.974 trillion. The 2023 numbers are shares of the U.S. credit card market only, total purchase volume $5.8 trillion. Subtracting one from the other to get a “+X pt” change is not meaningful. Both are presented below as separate reference points.

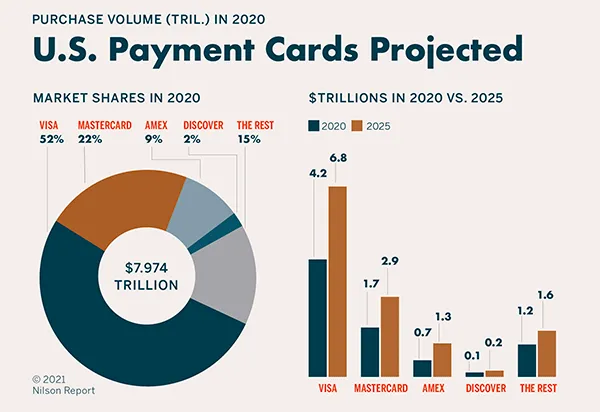

2020: U.S. Payment Cards (overall, $7.974T)

The 2020 U.S. share from the Nilson Report chart originally embedded in this article — purchase-volume basis, including credit, debit and prepaid — looked like this. “The Rest” (regional and other networks) made up 15%.

| Network | 2020 share (Payment Cards overall) |

|---|---|

| Visa | 52% |

| Mastercard | 22% |

| AmEx | 9% |

| Discover | 2% |

| The Rest | 15% |

| Total | 100% (base $7.974T) |

2023: U.S. credit cards only ($5.8T)

The 2023 figures, sourced from a Motley Fool article citing Nilson Report, cover the credit-card market only, base $5.8 trillion. Because UnionPay and JCB are essentially absent from the U.S. credit card market, the four-network total adds up to 100%.

| Network | 2023 share (credit cards only) |

|---|---|

| Visa | 52% |

| Mastercard | 24% |

| AmEx | 19% |

| Discover | 5% |

| Total | 100% (base $5.8T, credit cards only) |

- 2020 (Payment Cards overall): Visa leads at 52%. Mastercard 22%, AmEx 9%, Discover 2%, with The Rest at 15%. This is the all-of-payment-cards picture (credit + debit + prepaid).

- 2023 (credit cards only): Visa 52%, Mastercard 24%, AmEx 19%, Discover 5%, summing to 100%. Within the credit card market AmEx looks larger.

- Per-brand point differences cannot be subtracted across the two years. The base and the totals are different, so claims like “Mastercard +2 pt” or “AmEx +10 pt” do not hold up. Each year should be read on its own terms.

The original 2020 chart image is kept here for reference.

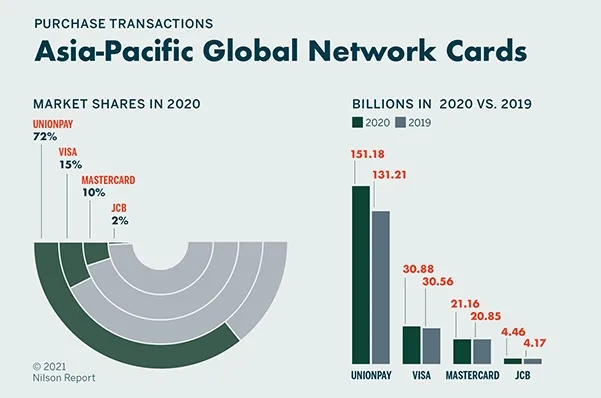

Asia Pacific: UnionPay dominance continues

The 2020 Nilson Report figures for Asia Pacific, on a transactions basis:

| Network | 2020 share | 2024-2025 estimate (reference) | Change |

|---|---|---|---|

| UnionPay | 72% | approx. 70% | -2 pt (still very high) |

| Visa | 15% | gradual growth | slight expansion |

| Mastercard | 10% | small increase | slight expansion |

| JCB | 2% | around 2% | roughly flat |

The size of the Chinese market keeps UnionPay’s regional dominance largely intact in 2024-2025. Visa and Mastercard grow gradually, but the overall structure does not shift much. JCB stays in the 2% band on a transactions basis in published references.

If you narrow the view to Japan only, JCB’s footprint is much larger. At the regional level, however, Chinese market scale dominates the picture in 2026 just as it did in 2020.

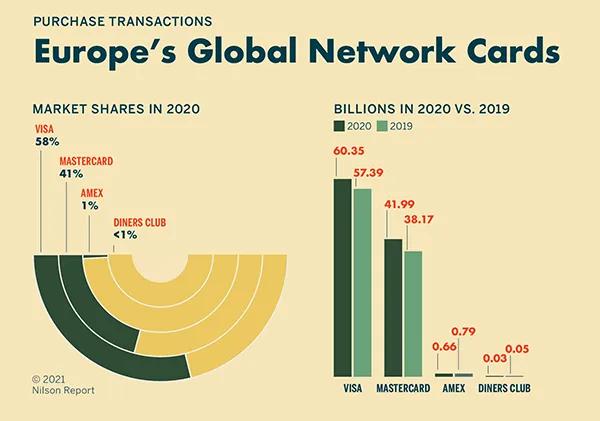

Europe: the “Mastercard myth” is fading

Where did the “Mastercard myth” come from in the first place? Travel guides and personal blogs — especially when I was reading up on overseas trips years ago — used to say “if you are going to Europe, carry one Mastercard.” The usual explanation is that Mastercard absorbed the European debit brand Maestro and the older Eurocard, ending up embedded in many European bank-issued cards. I have not personally verified this lineage, so treat the historical context as background colour rather than a confirmed fact.

The 2020 transactions-share picture for Europe was already this:

| Network | 2020 share | 2024-2025 published estimate | Change |

|---|---|---|---|

| Visa | 58% | approx. 51% | -7 pt |

| Mastercard | 41% | approx. 47% (estimate) | +6 pt |

| AmEx | 1% | low single digits | roughly flat |

| Diners Club | <1% | <1% | roughly flat |

A point that often gets missed: even back in 2020, Visa was already ahead in Europe at 58%, with Mastercard at 41%. The “Europe equals Mastercard” intuition was, statistically, already off. The 2024-2025 published estimates put Visa at roughly 51% and Mastercard at roughly 47%. These are estimates from secondary sources such as Statista rather than first-party Nilson public data, so they are best treated as reference values. The takeaway in 2026 is that Visa is still ahead in Europe, but the gap to Mastercard has narrowed.

That said, Europe is heterogeneous at the country level — Mastercard is still strong in some markets. The practical heuristic “Visa alone usually works in Europe” remains valid, much as it did in 2020.

Summary of regional changes

- United States: Visa leads at the 52% level both in 2020 (Payment Cards overall) and in 2023 (credit cards only). The bases differ, so per-brand point changes cannot be compared between the two years; each is a separate reference point.

- Asia Pacific: UnionPay dominance continues, driven by Chinese market scale.

- Europe: Visa still ahead, but Mastercard has narrowed the gap (Visa around 51% / Mastercard around 47%). The “Europe equals Mastercard” framing is outdated.

JCB sits outside the global Big Three, but its scale has expanded steadily over the past five years.

2020 vs 2025

JCB’s scale indicators across a five-year window (source: JCB global site “What we do”, figures as of end-September 2025):

| Indicator | 2020 (estimate) | End-September 2025 | Change |

|---|---|---|---|

| Merchant locations (global) | approx. 37 million | approx. 71 million | +approx. 34 million / about 1.9x |

| Cardmembers | approx. 140 million | over 175 million | +approx. 35 million / about 1.25x |

| Annual transaction volume | approx. JPY 35 trillion range | over JPY 50 trillion (FY2024 figure published as of end-March 2025) | not published on the global site as of end-September 2025 |

The merchant figure includes acceptance via reciprocal agreements with Discover and Diners Club. Even so, the five-year scale expansion is clear. Regional share figures (around 2% on a transactions basis in Asia Pacific) have not moved much, however, so the global Big Three still represents a hard wall in raw share terms.

The April 2023 acquirer fee revision changed the picture

A weak point I wrote about in the 2022 version — “JCB has higher acquirer fees, and you sometimes hit shops or online services where JCB is not accepted” — has improved in part. In April 2023, Square reduced its in-person JCB processing rate from 3.95% to 3.25%. JCB’s own merchant payment service “JCB Link Plan” offers a flat 3.25% as well. The rate gap with Visa and Mastercard has narrowed in some channels, even if it is not a market-wide cut.

In daily-use terms, scenes where “only JCB does not work” still exist — particularly with overseas online stores and some subscription services — but they are fewer than they used to be.

My own setup (as of May 2026)

My main card is JCB The Class. In Japan domestic use, it works in roughly 95% of scenes without any issue. The spread of QUICPay has effectively eliminated the “JCB only is not accepted” experience at physical stores. For overseas online use I keep a Visa (Sumitomo Mitsui NL) as a backup.

What to look at when picking a network (with 2020 to 2026 changes)

Differences in overseas usability

When you actually use a credit card abroad, network differences matter. Acceptance varies by region in fairly clear-cut ways, so generalising across “Asia” as a single block is not useful in practice.

- JCB: Strong acceptance in destinations popular with Japanese travellers — Hawaii, Guam, Taiwan, South Korea.

- UnionPay: Dominant in mainland China, Hong Kong and Macau.

- Visa / Mastercard: Broad acceptance in the U.S., Europe and Australia.

A multi-network setup remains a sensible strategy in 2026. Compared to 2020, scenes where a Visa-only setup falls short have become even rarer. Visa stayed at the 52% level in the U.S. and remains ahead in Europe at around 51%, so for a single overseas card, Visa is the practical choice. JCB pairs well with travel patterns weighted toward Japan plus Hawaii, Guam, Taiwan and South Korea, with the JCB-affiliated lounges and Japanese-hotel benefits as additional perks.

Security and bundled insurance

These differ more by issuer than by network. American Express and Diners Club tend to bundle stronger travel insurance and lounge access. Visa and Mastercard provide similar perks at gold tier and above. In practice, card grade matters more than network choice for these dimensions.

Payment trends as of 2026

Beyond the network-level shifts, the broader payment landscape has changed since 2020.

- Touch payment is now mainstream at convenience stores and restaurants. SMBC NL’s 7% convenience-store reward, starting December 2025, applies only to smartphone touch payments and mobile-order use (details below).

- Mobile wallets run alongside physical cards. Apple Pay and Google Pay use of credit cards has become routine; carrying a physical card is no longer always necessary.

- QR-code payment is in parallel competition. PayPay, Rakuten Pay and similar services run alongside cards. Cards are still the core payment instrument but no longer the only one.

- Online services keep cards at the centre. Subscriptions and online services still default to credit cards.

The competitive picture is no longer just network-versus-network. The relevant question has shifted from “which network do I pick” to “which payment methods do I combine”.

Sumitomo Mitsui NL 7% reward: what changed in 2025-2026

The original article said “Sumitomo Mitsui Card Visa (NL) gives up to 7% reward on convenience-store touch payments.” Two changes landed close together: one in December 2025, and another in February 2026, redefining both eligible payment methods and maximum reward rates.

To put it in order:

- Through November 2025: 7% reward at convenience stores and restaurants, on either physical-card or smartphone touch payment.

- From December 2025: Eligible methods narrowed to “smartphone touch payment” and “mobile order”. Physical-card touch payment is no longer eligible.

- From February 2026: Olive Flexible Pay’s credit mode reaches 8%; standalone NL and NL Gold remain at 7%. Olive’s debit mode is at 1.5%.

For someone like me using NL Gold standalone (without Olive), the rate stays at 7%. The change to be aware of from December 2025 onward is the need to switch to smartphone touch payment via Apple Pay or Google Pay to remain eligible for the 7% rate.

The official source is the Sumitomo Mitsui Card site.

Practical card choice in Japan

When picking cards in Japan, the relevant trade-offs are: overseas usability, the desire to support a Japanese brand, and concrete reward-rate economics.

The pitfall to avoid is holding too many cards and spreading rewards too thin. Splitting transactions across many cards leads to scattered reward balances, missed expiry dates, and effectively unspent value.

My setup is one card per major network:

- Main: JCB (ORIGINAL series, The Class)

- Sub: Visa (Sumitomo Mitsui NL Gold)

- Sub-sub: Mastercard (Rakuten Card) — used only for Rakuten Ichiba and Rakuten furusato nozei

The full rationale and use-case split is documented separately (Japanese article).

If you want a Japanese brand: JCB

JCB is the only Japan-origin global network. I use it as my main card.

JCB still has gaps in some specific cases. In day-to-day domestic use, my experience is roughly 95% smooth. The remaining gap shows up on overseas online checkout pages where JCB is not offered.

QUICPay adoption has effectively removed the “physical store does not take JCB” issue. The “overseas online does not take JCB” issue has improved but is not gone in 2026. Backing it up with a Visa is the realistic setup.

If global usability matters: Visa

Visa was the safe default in 2020, and that has not changed in 2026. Visa stays at the 52% level in the U.S., and the Visa lead in Europe continues even as Mastercard narrows the gap. The overall “Visa-dominant” structure persists.

For my Visa slot, I use Sumitomo Mitsui Card Visa (NL Gold). The 7% convenience-store reward via smartphone touch payment lands in everyday spend.

Note: The screenshot above is from SMBC’s official Japanese marketing site and remains in Japanese. The summary above this image describes the same rate changes in English.

Reference: site information as of 2024/08/31, https://www.smbc-card.com/nyukai/merit/proper_p5.jsp

Summary

A summary of how credit-card network share has and has not changed between 2020 and 2024-2025 published data:

- The “Big Five vs Big Seven” naming aside, Visa, Mastercard and UnionPay together hold roughly 97% of global purchase transactions.

- The U.S. has Visa leading at the 52% level both in 2020 (Payment Cards overall) and in 2023 (credit cards only). The two bases differ, so direct point comparisons are not valid, but Visa’s regional lead is consistent. Europe still has Visa ahead, with Mastercard narrowing the gap. Asia Pacific remains UnionPay-dominant.

- JCB has grown to about 71 million merchant locations and over 175 million cardmembers (as of end-September 2025), but its share in regional transaction-share figures has barely moved.

- Sumitomo Mitsui’s NL 7% reward, from December 2025 onward, requires switching to smartphone touch payment rather than physical-card touch payment.

For everyday life in Japan, having a single Visa is enough to cover most situations. Adding a JCB as a secondary card avoids the small remaining gaps in domestic acceptance. JCB’s 2023 acquirer fee revisions have improved its position structurally; outside overseas online checkouts, it is more usable than it was in 2020.

FAQ

JCB or Visa — which is better?

The safer default is Visa. It is more consistently accepted overseas and in overseas online checkouts. JCB is a stronger pick when the priorities are Japan domestic use, Asian travel and JCB-specific perks such as JCB-affiliated lounges.

Visa or Mastercard — which is more usable?

Both have high enough acceptance that the practical difference is small. As of 2026, Visa has the higher global share: leading the U.S. at the 52% level and still leading Europe (around 51% versus Mastercard’s roughly 47%). A single Visa is sufficient for almost every practical scenario.

What is the role of a payment network?

Networks act as the global rails that let card transactions clear across regions. Issuers piggy-back on these networks to make their cards usable internationally.

Is UnionPay usable in Japan?

UnionPay-only cards are uncommon in Japan, and acceptance is concentrated in tourist areas and Chinese-affiliated stores. UnionPay’s global share is large — 33.2% of H1 2024 transactions, second only to Visa — but for Japan domestic use, Visa, Mastercard and JCB remain the practical core.

"Big Five" or "Big Seven" — which is correct?

Both groupings exist in industry references. The “Big Five” is Visa / Mastercard / JCB / AmEx / Diners Club. The “Big Seven” adds UnionPay and Discover; JCB’s official site lists seven brands, and this article uses the seven-brand framing. When the discussion is about share specifically, “Big Three” (Visa / Mastercard / UnionPay, roughly 97% combined) is often the more useful framing.

Sources

The primary and secondary sources referenced in this article:

- Nilson Report Archive of Charts & Graphs (2020 data — global, U.S., Europe, Asia Pacific):

https://nilsonreport.com/publication_chart_and_graphs_archive.php(link broken, returned 404 as of 2026-05) - Nilson Report “Global Brand Cards Worldwide — Midyear 2024” (global H1 2024 share): https://nilsonreport.com/articles/global-brand-cards-worldwide-midyear-2024/

- Motley Fool “Credit & Debit Card Market Share by Network and Issuer” (U.S. 2023 share / cards in circulation): https://www.fool.com/money/research/credit-debit-card-market-share-network-issuer/

- Europe 2024-2025 share (published estimates): public estimates such as those summarised on Statista. The exact URLs vary by year and subscription tier, so the article uses Visa around 51% / Mastercard around 47% as a reference value rather than first-party data.

- JCB global site, “What we do” (JCB merchant and cardmember figures, end-September 2025): https://www.global.jcb/en/about-us/what-we-do/

- Square press release (JCB in-person processing rate cut from 3.95% to 3.25%): https://squareup.com/jp/ja/press/jcb-processing-rate

- JCB Link Plan (flat 3.25%): https://www.jcb.co.jp/promotion/acq/webplan/index.html

- JCB official network comparison: https://www.jcb.co.jp/ordercard/special/international_brand.html

- Sumitomo Mitsui Card 7% / 8% reward: https://www.smbc-card.com/mem/cardinfo/cardinfo9001629.jsp